Volatility modelling: EWMA and GARCH

Contents

Volatility modelling: EWMA and GARCH#

Import the necessary packages

packages |

acronyms |

|---|---|

matplotlib.pyplot |

plt |

numpy |

np |

os |

|

pandas |

pd |

scipy.optimize |

spop |

import matplotlib.pyplot as plt

import numpy as np

import os

import pandas as pd

import scipy.optimize as spop

import warnings

warnings.simplefilter('ignore')

Set your working directory using

os.chdir([PATH])(change directory).

#os.chdir(r'C:\Users\cdes1\OneDrive - ICHEC\Documents\Cours\PortfolioManagement')

os.chdir(r'/Users/christophe/OneDrive - ICHEC/Documents/Cours/PortfolioManagement')

Check that the working directory has been updated (

os.getcwd()).

os.getcwd()

'/Users/christophe/Library/CloudStorage/OneDrive-ICHEC/Documents/Cours/PortfolioManagement'

S&P500#

Import the excel File

sp500_daily.xlsx(in yourdatafolder) as a DataFrame calleddf.

df = pd.read_excel('data/sp500_daily.xlsx', index_col=0, parse_dates=True)

Display the first 5 rows of this DataFrame (using

df.head()).

df.head()

| CLOSE | |

|---|---|

| Date | |

| 1930-01-02 | 21.18 |

| 1930-01-03 | 21.23 |

| 1930-01-04 | 21.48 |

| 1930-01-06 | 21.50 |

| 1930-01-07 | 21.31 |

Display the last 5 rows of this DataFrame (using

df.tail()).

df.tail()

| CLOSE | |

|---|---|

| Date | |

| 2022-12-23 | 3844.8150 |

| 2022-12-27 | 3829.2493 |

| 2022-12-28 | 3783.2219 |

| 2022-12-29 | 3849.2832 |

| 2022-12-30 | 3839.4966 |

Display some information about this DataFrame (using

df.info()).

df.info()

<class 'pandas.core.frame.DataFrame'>

DatetimeIndex: 24060 entries, 1930-01-02 to 2022-12-30

Data columns (total 1 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 CLOSE 24060 non-null float64

dtypes: float64(1)

memory usage: 375.9 KB

Rename the column “CLOSE” as “price”.

https://pandas.pydata.org/docs/reference/api/pandas.DataFrame.rename.html

df.rename(columns={'CLOSE': 'price'}, inplace=True)

df

| price | |

|---|---|

| Date | |

| 1930-01-02 | 21.1800 |

| 1930-01-03 | 21.2300 |

| 1930-01-04 | 21.4800 |

| 1930-01-06 | 21.5000 |

| 1930-01-07 | 21.3100 |

| ... | ... |

| 2022-12-23 | 3844.8150 |

| 2022-12-27 | 3829.2493 |

| 2022-12-28 | 3783.2219 |

| 2022-12-29 | 3849.2832 |

| 2022-12-30 | 3839.4966 |

24060 rows × 1 columns

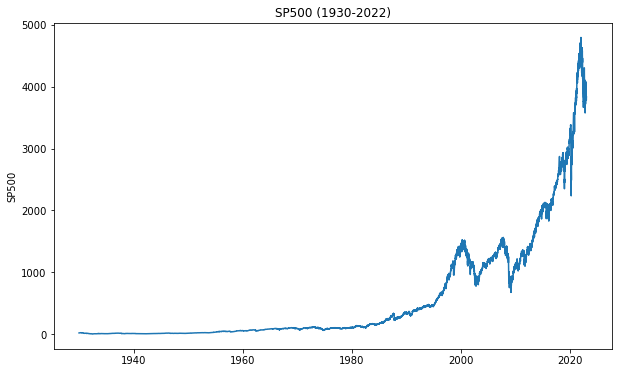

Line chart#

Create a line plot of the S&P500.

Set a label SP500 on the y-axis and a title (e.g., ’SP500 (1930-2022)’)

https://matplotlib.org/stable/gallery/index.html

Save this figure in your folder images.

fig, ax = plt.subplots(figsize=(10, 6))

ax.plot(df['price'])

# ax.plot(df) also works because there is only one column in the DataFrame

plt.ylabel('SP500')

plt.title('SP500 (1930-2022)')

fig.savefig('images/volatility_sp500.png')

plt.show()

Compute the logarithmic returns.

Remove the first missing row.

Rename the column “price” into “rets”

Display the first 5 rows.

rets = np.log(df / df.shift(1)).dropna() # rendement log

rets.rename(columns={'price': 'rets'}, inplace=True)

rets.head()

| rets | |

|---|---|

| Date | |

| 1930-01-03 | 0.002358 |

| 1930-01-04 | 0.011707 |

| 1930-01-06 | 0.000931 |

| 1930-01-07 | -0.008876 |

| 1930-01-08 | -0.000939 |

Compute the volatility

“Classical formula”: Volatility is computed as the standard deviation of the returns. To annualize volatility, multiply by the square root of data frequency.

historical_volatility = np.std(rets) * np.sqrt(252)

historical_volatility

rets 0.182536

dtype: float64

Note: the [0] is needed in order to only get the number.

historical_volatility = np.std(rets) * np.sqrt(252)

historical_volatility

rets 0.182536

dtype: float64

We can also use [‘rets’].

historical_volatility = np.std(rets) * np.sqrt(252)

historical_volatility['rets']

0.1825362035297431

Alternatively, we can use the .std() method on the DataFrame.

rets.std() * np.sqrt(252)

rets 0.18254

dtype: float64

Finally, a nice output, we can use format.

historical_volatility = np.std(rets) * np.sqrt(252)

historical_volatility = historical_volatility['rets']

print("{:.4%}".format(historical_volatility))

18.2536%

“Finance formula”: We can also make the simplifying assumption that \(\bar{r} = 0\). In this case, the variance is simply the sum of the squared returns.

historical_volatility = np.sqrt(np.mean(rets**2, axis=0)) * np.sqrt(252)

historical_volatility = historical_volatility[0]

print("{:.4%}".format(historical_volatility))

18.2568%

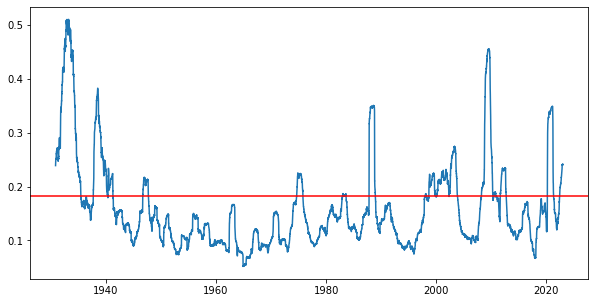

Rolling volatility

Volatility is not constant. Let’s compute it and plot it using a rolling window of 252 days (approximately 1 year).

rolling_vol = (rets.rolling(252).std()*np.sqrt(252))

fig, ax = plt.subplots(figsize=(10,5))

ax.plot(rolling_vol)

plt.axhline(historical_volatility, color='red')

plt.savefig('images/volatility_rolling_window_volatility.png')

plt.show();

EWMA#

Using the returns from 2010, use the EWMA to model volatility

To make things visual, we will put everything inside the DataFrame, very similar to what we would have done in Excel.

rets = rets.loc['2010-01-01':].copy()

rets.head()

| rets | |

|---|---|

| Date | |

| 2010-01-04 | 0.015910 |

| 2010-01-05 | 0.003118 |

| 2010-01-06 | 0.000540 |

| 2010-01-07 | 0.004000 |

| 2010-01-08 | 0.002876 |

Compute the number of observations and store this value in n.

n = rets.shape[0]

n

3272

Compute the squared returns and store it in a new column rets_sq.

rets['rets_sq'] = rets['rets']**2

rets

| rets | rets_sq | |

|---|---|---|

| Date | ||

| 2010-01-04 | 0.015910 | 2.531178e-04 |

| 2010-01-05 | 0.003118 | 9.720487e-06 |

| 2010-01-06 | 0.000540 | 2.920861e-07 |

| 2010-01-07 | 0.004000 | 1.599607e-05 |

| 2010-01-08 | 0.002876 | 8.271171e-06 |

| ... | ... | ... |

| 2022-12-23 | 0.005850 | 3.422799e-05 |

| 2022-12-27 | -0.004057 | 1.645688e-05 |

| 2022-12-28 | -0.012093 | 1.462353e-04 |

| 2022-12-29 | 0.017311 | 2.996689e-04 |

| 2022-12-30 | -0.002546 | 6.480512e-06 |

3272 rows × 2 columns

Create a vector conditional of zero’s with size n and add this vector in a column conditional.

conditional = np.zeros(n)

rets['conditional'] = conditional

rets

| rets | rets_sq | conditional | |

|---|---|---|---|

| Date | |||

| 2010-01-04 | 0.015910 | 2.531178e-04 | 0.0 |

| 2010-01-05 | 0.003118 | 9.720487e-06 | 0.0 |

| 2010-01-06 | 0.000540 | 2.920861e-07 | 0.0 |

| 2010-01-07 | 0.004000 | 1.599607e-05 | 0.0 |

| 2010-01-08 | 0.002876 | 8.271171e-06 | 0.0 |

| ... | ... | ... | ... |

| 2022-12-23 | 0.005850 | 3.422799e-05 | 0.0 |

| 2022-12-27 | -0.004057 | 1.645688e-05 | 0.0 |

| 2022-12-28 | -0.012093 | 1.462353e-04 | 0.0 |

| 2022-12-29 | 0.017311 | 2.996689e-04 | 0.0 |

| 2022-12-30 | -0.002546 | 6.480512e-06 | 0.0 |

3272 rows × 3 columns

Initialize the second value as the squared value of the first return.

# rets.iloc[1]['conditional'] = rets.iloc[0]['rets']**2

# this results in a warning

rets.loc[rets.index[1], 'conditional'] = rets.iloc[0]['rets_sq']

rets

| rets | rets_sq | conditional | |

|---|---|---|---|

| Date | |||

| 2010-01-04 | 0.015910 | 2.531178e-04 | 0.000000 |

| 2010-01-05 | 0.003118 | 9.720487e-06 | 0.000253 |

| 2010-01-06 | 0.000540 | 2.920861e-07 | 0.000000 |

| 2010-01-07 | 0.004000 | 1.599607e-05 | 0.000000 |

| 2010-01-08 | 0.002876 | 8.271171e-06 | 0.000000 |

| ... | ... | ... | ... |

| 2022-12-23 | 0.005850 | 3.422799e-05 | 0.000000 |

| 2022-12-27 | -0.004057 | 1.645688e-05 | 0.000000 |

| 2022-12-28 | -0.012093 | 1.462353e-04 | 0.000000 |

| 2022-12-29 | 0.017311 | 2.996689e-04 | 0.000000 |

| 2022-12-30 | -0.002546 | 6.480512e-06 | 0.000000 |

3272 rows × 3 columns

Initialize a variable lambda_val with a value of 0.94. Then, implement this formula:

Note 1: lambda cannot be used as variable name as it has another signification in Python.

Note 2: the vector rets has one additional observation in comparison to the vector conditional.

lambda_val = 0.94

for t in range(2, n):

rets.loc[rets.index[t], 'conditional'] = lambda_val * rets.iloc[t-1]['conditional'] \

+ (1 - lambda_val) * rets.iloc[t-1]['rets'] ** 2

rets.head()

| rets | rets_sq | conditional | |

|---|---|---|---|

| Date | |||

| 2010-01-04 | 0.015910 | 2.531178e-04 | 0.000000 |

| 2010-01-05 | 0.003118 | 9.720487e-06 | 0.000253 |

| 2010-01-06 | 0.000540 | 2.920861e-07 | 0.000239 |

| 2010-01-07 | 0.004000 | 1.599607e-05 | 0.000224 |

| 2010-01-08 | 0.002876 | 8.271171e-06 | 0.000212 |

Compute the loglikelihood as:

where:

\(u_i\): return

\(v_i\): conditional

rets.loc[rets.index[1:], 'likelihood'] = -np.log(rets.iloc[1:]['conditional']) \

-((rets.iloc[1:]['rets']**2)/rets.iloc[1:]['conditional'])

rets.head()

| rets | rets_sq | conditional | likelihood | |

|---|---|---|---|---|

| Date | ||||

| 2010-01-04 | 0.015910 | 2.531178e-04 | 0.000000 | NaN |

| 2010-01-05 | 0.003118 | 9.720487e-06 | 0.000253 | 8.243253 |

| 2010-01-06 | 0.000540 | 2.920861e-07 | 0.000239 | 8.339858 |

| 2010-01-07 | 0.004000 | 1.599607e-05 | 0.000224 | 8.331539 |

| 2010-01-08 | 0.002876 | 8.271171e-06 | 0.000212 | 8.421147 |

Compute the sum of the log-likelihood into log_likelihood.

log_likelihood = rets['likelihood'].sum()

log_likelihood

27407.697995474882

Wrap everything within a function ewma_pandas, which takes two arguments: (1) the value of the lambda (lambda_val) and (2) the returns. This function returns the value of the loglikelihood.

def ewma_pandas(lambda_val, rets):

df = rets.copy()

n = df.shape[0]

df['rets_sq'] = df['rets']**2

conditional = np.zeros(n)

df['conditional'] = conditional

df.loc[df.index[1], 'conditional'] = df.iloc[0]['rets']**2

for t in range(2, n):

df.loc[df.index[t], 'conditional'] = lambda_val * df.iloc[t-1]['conditional'] \

+ (1 - lambda_val) * df.iloc[t-1]['rets'] ** 2

df.loc[df.index[1:], 'likelihood'] = -np.log(df.iloc[1:]['conditional']) \

-((df.iloc[1:]['rets']**2)/df.iloc[1:]['conditional'])

log_likelihood = df['likelihood'].sum()

return -log_likelihood

df = pd.read_excel('data/sp500_daily.xlsx', index_col=0, parse_dates=True)

rets = np.log(df/df.shift(1)).dropna()

rets.rename(columns={'CLOSE':'rets'}, inplace=True)

rets = rets.loc['2010-01-01':]

rets

| rets | |

|---|---|

| Date | |

| 2010-01-04 | 0.015910 |

| 2010-01-05 | 0.003118 |

| 2010-01-06 | 0.000540 |

| 2010-01-07 | 0.004000 |

| 2010-01-08 | 0.002876 |

| ... | ... |

| 2022-12-23 | 0.005850 |

| 2022-12-27 | -0.004057 |

| 2022-12-28 | -0.012093 |

| 2022-12-29 | 0.017311 |

| 2022-12-30 | -0.002546 |

3272 rows × 1 columns

Call this function with a lambda value of 0.94. You should find the same value.

rets

ewma_pandas(0.94, rets)

-27407.697995474882

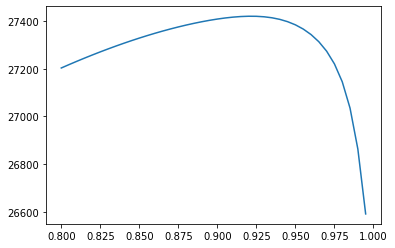

Naive optimization#

For different values of lambda between 0.80 and 1.00, compute the value of the different loglikelihood and plot it.

lambda_vals = np.arange(0.80, 1, 0.005)

log_vals = [-ewma_pandas(lam, rets) for lam in lambda_vals]

plt.plot(lambda_vals, log_vals);

We notice a maximum around 0.925. Let’s now optimize it to find the actual answer.

# reinitialize dataframe

rets = np.log(df / df.shift(1)).dropna() # rendement log

rets.rename(columns={'CLOSE': 'rets'}, inplace=True)

rets = rets.loc['2010-01-01':].copy()

var = np.std(rets)**2 # historical variance

res = spop.minimize(ewma_pandas, var, rets, method="Nelder-Mead")

params = res.x

function = res.fun

print('Parameters: ', res.x)

print('LogLikelihood: ', -res.fun)

Parameters: [0.92171991]

LogLikelihood: 27420.928807446242

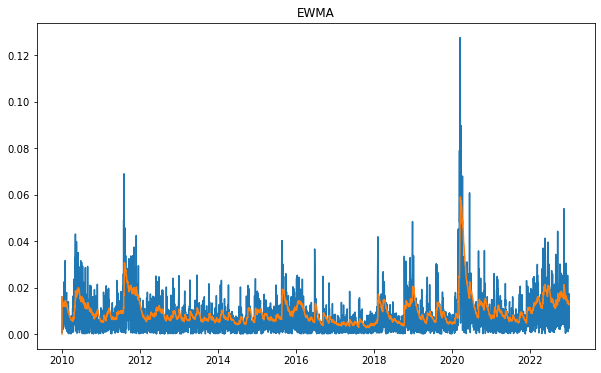

lambda_val = res.x

df = rets.copy()

n = df.shape[0]

df['rets_sq'] = df['rets']**2

conditional = np.zeros(n)

df['conditional'] = conditional

df.loc[df.index[1], 'conditional'] = df.iloc[0]['rets']**2

for t in range(2, n):

df.loc[df.index[t], 'conditional'] = lambda_val * df.iloc[t-1]['conditional'] \

+ (1 - lambda_val) * df.iloc[t-1]['rets'] ** 2

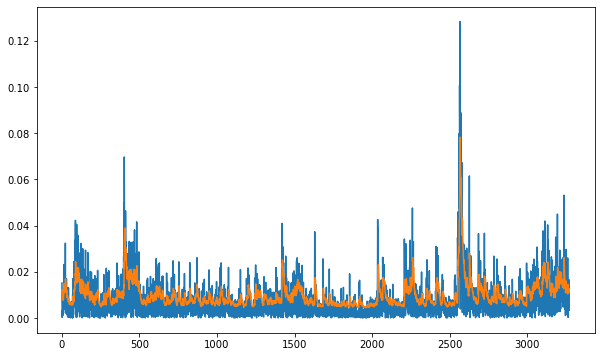

fig, ax = plt.subplots(figsize=(10,6))

ax.plot(np.abs(df['rets']))

ax.plot(df['conditional']**(1/2))

ax.set_title('EWMA')

plt.show()

%%time

ewma_pandas(0.94, rets)

CPU times: user 447 ms, sys: 1.57 ms, total: 449 ms

Wall time: 448 ms

-27407.697995474882

Improve performance using numpy#

It is not easy nor efficient to fill a DataFrame. A better approach (although less beautiful) is to work with numpy arrays. Reimplement everything without using Pandas.

df = pd.read_excel('data/sp500_daily.xlsx', index_col=0, parse_dates=True)

rets = np.log(df / df.shift(1)).dropna() # rendement log

rets.rename(columns={'CLOSE': 'rets'}, inplace=True)

rets = rets.loc['2010-01-01':]

rets = np.array(rets).ravel()

rets.shape

rets

array([ 0.01590968, 0.00311777, 0.00054045, ..., -0.01209278,

0.01731095, -0.00254568])

n = len(rets)

n

3272

conditional = np.zeros(n-1)

conditional[0] = rets[0]**2

conditional

array([0.00025312, 0. , 0. , ..., 0. , 0. ,

0. ])

lambda_val = 0.94

for t in range(1, len(conditional)):

conditional[t] = lambda_val * conditional[t-1] + (1 - lambda_val) * rets[t] ** 2

conditional

array([0.00025312, 0.00023851, 0.00022422, ..., 0.00017394, 0.00017228,

0.00017992])

likelihood = -np.log(conditional)-((rets[1:]**2)/conditional)

likelihood

array([8.24325261, 8.33985817, 8.33153924, ..., 7.81607462, 6.92696348,

8.58695739])

log_likelihood = np.sum(likelihood)

log_likelihood

27407.697995474882

It’s now time to wrap everything within a function ewma. We assume that we pass to the function two arguments:

the value of the lambda

a series of return in a ndarray

rets = np.array(rets)

def ewma_numpy(lambda_val, rets):

n = len(rets)

conditional = np.zeros(n-1)

conditional[0] = rets[0]**2

for t in range(1, len(conditional)):

conditional[t] = lambda_val * conditional[t-1] + (1 - lambda_val) * rets[t] ** 2

likelihood = -np.log(conditional)-((rets[1:]**2)/conditional)

log_likelihood = np.sum(likelihood)

return -log_likelihood

Let’s check we get the same value of the logLikelihood using the function.

%%time

ewma_numpy(lambda_val=0.94, rets=rets)

CPU times: user 2.42 ms, sys: 269 µs, total: 2.69 ms

Wall time: 2.49 ms

-27407.697995474882

It’s now time to optimize the function using spop.minimize.

var = np.std(rets)**2 # historical variance

res = spop.minimize(ewma_numpy, [var], rets, method="Nelder-Mead")

params = res.x

function = res.fun

print('Parameters: ', res.x)

print('LogLikelihood: ', -res.fun)

Parameters: [0.92171991]

LogLikelihood: 27420.928807446242

GARCH Modelling (NEDL)#

Now it’s your turn to implement the GARCH method.

df = pd.read_excel('data/sp500_daily.xlsx', index_col=0, parse_dates=True)

rets = np.log(df / df.shift(1)).dropna()

rets.rename(columns={'CLOSE': 'rets'}, inplace=True)

rets = rets.loc['2010-01-01':].copy()

rets = np.array(rets)

rets = rets.ravel()

mean = np.average(rets)

var = np.var(rets)

def garch_nedl(params):

mu = params[0]

omega = params[1]

alpha = params[2]

beta = params[3]

long_run = (omega/(1-alpha-beta))**(1/2)

resid = rets - mu

realised = abs(resid)

conditional = np.zeros(len(rets))

conditional[0] = long_run

for t in range(1, len(rets)):

conditional[t] = (omega + alpha*resid[t-1]**2 + beta*conditional[t-1]**2)**(1/2)

likelihood = 1/((2*np.pi)**(1/2)*conditional)*np.exp(-realised**2/(2*conditional**2))

log_likelihood = np.sum(np.log(likelihood))

return -log_likelihood

#bnds = tuple((0,1) for x in range(4))

res = spop.minimize(garch_nedl, [mean, var, 0, 0],

#bounds=bnds,

method='Nelder-Mead')

params = res.x

mu = params[0]

omega = params[1]

alpha = params[2]

beta = params[3]

long_run = (omega/(1-alpha-beta))**(1/2)

resid = rets - mu

realised = abs(resid)

conditional = np.zeros(len(rets))

conditional[0] = long_run

for t in range(1, len(rets)):

conditional[t] = (omega + alpha*resid[t-1]**2 + beta*conditional[t-1]**2)**(1/2)

print('GARCH model parameters')

print('----------------------')

print('mu', str(round(mu, 6)))

print('omega', str(round(omega, 6)))

print('alpha', str(round(alpha, 6)))

print('beta', str(round(beta, 6)))

GARCH model parameters

----------------------

mu 0.000775

omega 4e-06

alpha 0.178418

beta 0.793665

fig, ax = plt.subplots(figsize=(10, 6))

ax.plot(realised)

ax.plot(conditional)

[<matplotlib.lines.Line2D at 0x7fb3d8e45580>]

Garch zero-mean#

def garch_zero_mean(params):

# specifying model parameters

mu = 0

omega = params[0]

alpha = params[1]

beta = params[2]

# calculating long run volatility

# long_run = (omega/(1 - alpha - beta))**(1/2)

# calculating realized and conditional volatility

resid = rets - mu

realized = abs(resid)

conditional = np.zeros(len(rets))

conditional[0] = rets[0]**2

for t in range(1, len(rets)):

conditional[t] = (omega + alpha*resid[t-1]**2 + beta*conditional[t-1])

# calculating loglikelihood

likelihood = -np.log(conditional) - realized**2 / conditional

log_likelihood = np.sum(likelihood)

return -log_likelihood

#mean = np.average(returns)

var = np.std(rets)**2

bounds = [(0.0, 1.0)]*3

res = spop.minimize(garch_zero_mean, [var, 0, 0], bounds=bounds, method='Nelder-Mead')

mu = 0

omega = res.x[0]

alpha = res.x[1]

beta = res.x[2]

log_likelihood = -float(res.fun)

# calculating realized and conditional volatility

# long_run = (omega/(1 - alpha - beta))**(1/2)

resid = rets - mu

realized = abs(resid)

conditional = np.zeros(len(rets))

conditional[0] = rets[0]**2

for t in range(1, len(rets)):

conditional[t] = (omega + alpha*resid[t-1]**2 + beta*conditional[t-1]**2)**(1/2)

likelihood = -np.log(conditional) - realized**2 / conditional

log_likelihood = np.sum(likelihood)

print('GARCH model parameters')

print('----------------------')

print('mu', str(round(mu, 6)))

print('omega', str(round(omega, 6)))

print('alpha', str(round(alpha, 6)))

print('beta', str(round(beta, 6)))

# print('long-run volatility', str(round(long_run, 4)))

print('log-likelihood', str(round(log_likelihood, 4)))

GARCH model parameters

----------------------

mu 0

omega 7.7e-05

alpha 0.385073

beta 0.0

log-likelihood 14968.3621

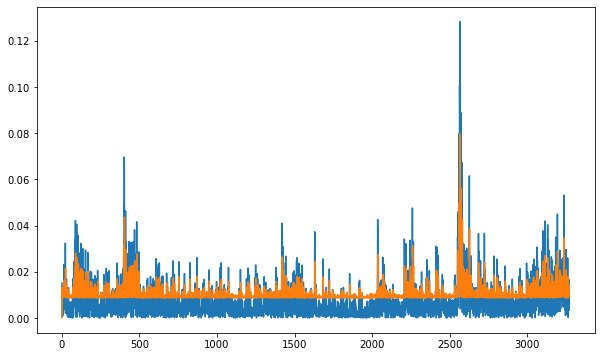

fig, ax = plt.subplots(figsize=(10, 6))

ax.plot(realised)

ax.plot(conditional)

[<matplotlib.lines.Line2D at 0x7fb3d8cddf70>]

ARCH package#

https://arch.readthedocs.io/en/latest/index.html

# !pip install arch

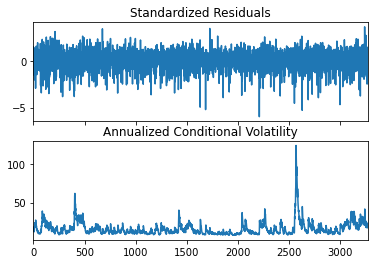

from arch import arch_model

am = arch_model(rets*100)

res = am.fit()

print(res.summary())

Iteration: 1, Func. Count: 6, Neg. LLF: 45190.138944107726

Iteration: 2, Func. Count: 17, Neg. LLF: 19000.159297830152

Iteration: 3, Func. Count: 27, Neg. LLF: 6719.894415448125

Iteration: 4, Func. Count: 34, Neg. LLF: 8186.897239907136

Iteration: 5, Func. Count: 40, Neg. LLF: 4525.832689694671

Iteration: 6, Func. Count: 47, Neg. LLF: 4243.099399974918

Iteration: 7, Func. Count: 53, Neg. LLF: 4241.2416896886125

Iteration: 8, Func. Count: 58, Neg. LLF: 4241.24076531225

Iteration: 9, Func. Count: 63, Neg. LLF: 4241.240763542724

Iteration: 10, Func. Count: 67, Neg. LLF: 4241.240763542601

Optimization terminated successfully (Exit mode 0)

Current function value: 4241.240763542724

Iterations: 10

Function evaluations: 67

Gradient evaluations: 10

Constant Mean - GARCH Model Results

==============================================================================

Dep. Variable: y R-squared: 0.000

Mean Model: Constant Mean Adj. R-squared: 0.000

Vol Model: GARCH Log-Likelihood: -4241.24

Distribution: Normal AIC: 8490.48

Method: Maximum Likelihood BIC: 8514.85

No. Observations: 3272

Date: Thu, Apr 06 2023 Df Residuals: 3271

Time: 16:11:37 Df Model: 1

Mean Model

==========================================================================

coef std err t P>|t| 95.0% Conf. Int.

--------------------------------------------------------------------------

mu 0.0776 1.326e-02 5.857 4.708e-09 [5.166e-02, 0.104]

Volatility Model

============================================================================

coef std err t P>|t| 95.0% Conf. Int.

----------------------------------------------------------------------------

omega 0.0369 7.769e-03 4.744 2.100e-06 [2.163e-02,5.208e-02]

alpha[1] 0.1801 2.365e-02 7.616 2.609e-14 [ 0.134, 0.226]

beta[1] 0.7932 2.206e-02 35.960 3.542e-283 [ 0.750, 0.836]

============================================================================

Covariance estimator: robust

fig = res.plot(annualize="D")

References and further ressources#

NEDL - ARCH model - volatility persistence in time series (Excel)

https://www.youtube.com/watch?v=-G5g3ChktEs

NEDL - GARCH model - volatility persistence in time series (Excel)

https://www.youtube.com/watch?v=88oOzPFVWTU

NEDL - GARCH model in Python